Impact of investing

From ambiguity to credibility: How to define sustainable investments in 2024

With the EU reevaluating SFDR regulations, Article 8 funds encountering heightened scrutiny, and the upcoming introduction of UK SDR regulation, it’s getting harder and harder for investors to keep up with how to actually define sustainable investments in 2024. To bring clarity, we explore three key definitions, navigating the pros and cons they throw at investors.

Published Mar 28, 2024

Published: March 2024

Sustainable investing has witnessed significant growth in recent years, both in terms of allocated capital and public attention. Alongside this surge, various regulatory and non-regulatory frameworks have emerged, offering high-level guidance on classifying sustainable investments. Notably, the EU's SFDR and the upcoming UK's SDR aim to enhance transparency and help redirect capital towards more sustainable assets.

Despite the high activity in classifying funds as sustainable after the introduction of the SFDR, the market has experienced a great deal of uncertainty on what truly constitutes a sustainable investment and how it can be measured.

For instance, according to a report by Morningstar, a staggering 55% of EU funds currently bear the Article 8 (“light green”) label. However, upon closer inspection of disclosure reports, Article 8 funds often merely implement exclusion criteria, for example abstaining from activities like controversial weapons and tobacco. In contrast, the more ambitious Article 9 label accounts for only 4% of EU funds, reflecting recent fund downgrades and unsuccessful attempts to clarify the definition of sustainable investment.

As regulatory authorities continue to further iterate sustainable investment frameworks and asset managers revisit their internal approaches, the central question remains unanswered: What truly defines a sustainable investment? Is it sufficient for a company to abstain from producing obviously harmful products to be deemed sustainable, or should the ambition level be set higher?

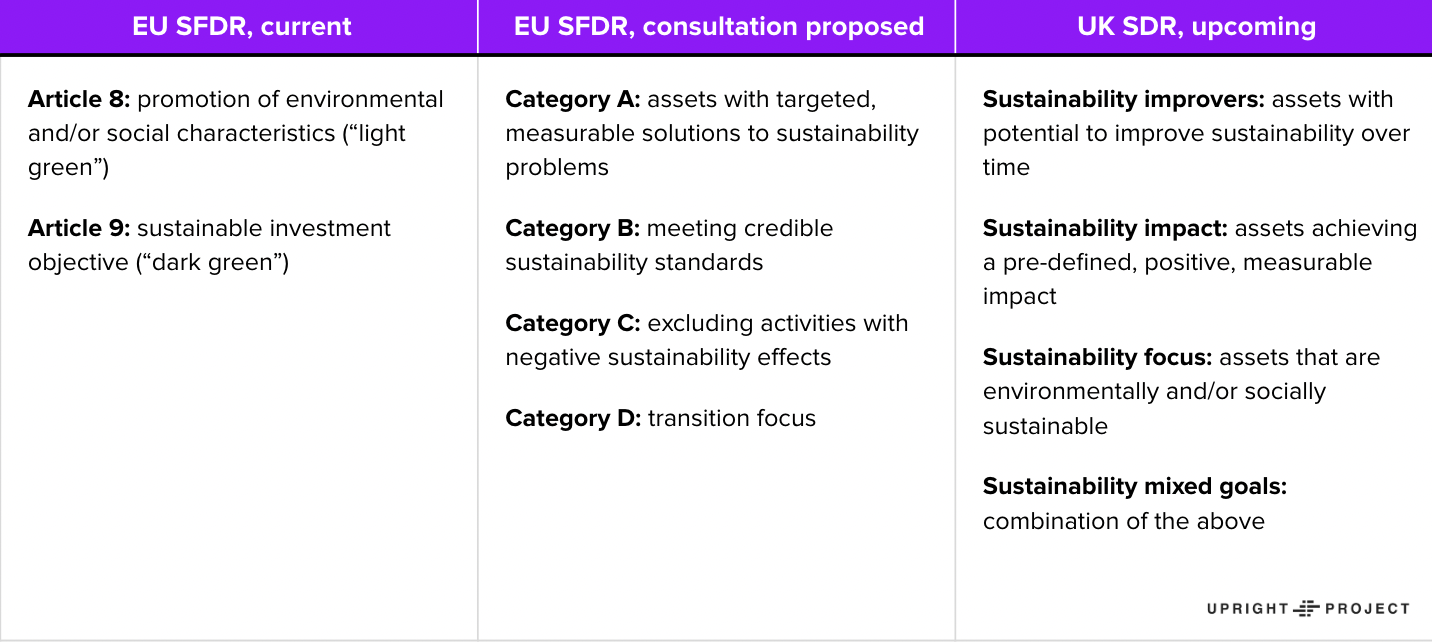

Here are examples of recent frameworks for sustainable investment classification and their category definitions:

Our analysis: The pros and cons of the three key definitions of sustainable investments

Setting aside fund labels, let's delve into what it could truly mean for an investment to be considered sustainable – focusing on the perspective of an individual investee company.

At Upright, we work daily with professional investors trying to find the right ways to define sustainable investments. Through exploration of current market practices and numerous discussions with industry stakeholders over the years, we have identified three overarching definitions to approach this topic.

Spoiler alert: Incremental reductions to CO2 don't yet make a company a sustainable investment target.

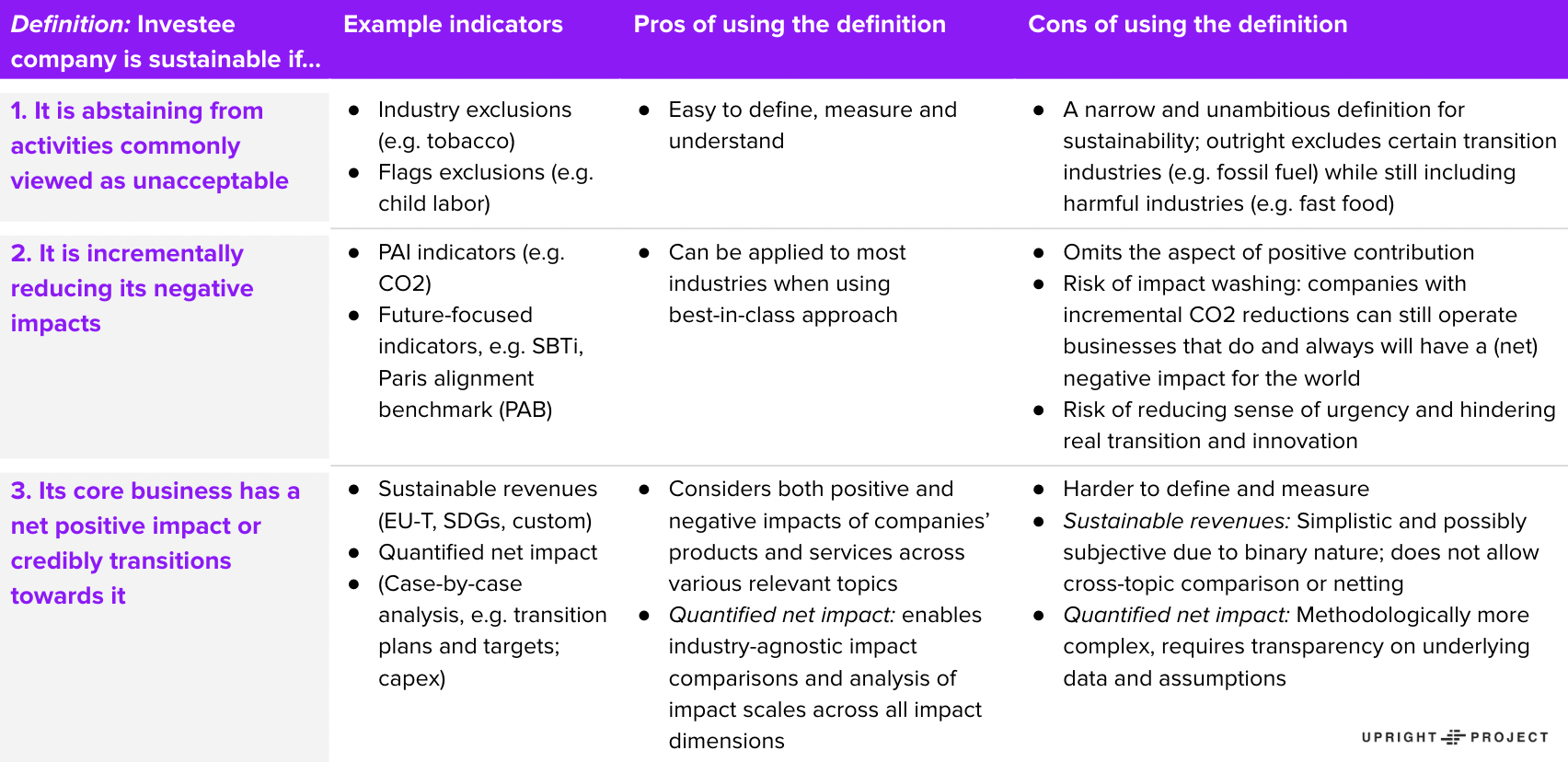

Here are three different ways to define a sustainable investment:

Next, let’s look at each type of definition a little closer. Spoiler alert: Incremental reductions to CO2 don’t make a company a sustainable investment target.

Definition 1: Exclusionary criteria

As evidenced by the popularity of Article 8 funds, the practice of viewing sustainability through exclusions has persisted over time and remains prevalent. This approach typically involves categorizing companies engaged in unacceptable industries or practices, such as tobacco or child labor, as unsustainable and excluding them from investment portfolios.

However, relying solely on exclusionary criteria presents a notable challenge: the ambition level for sustainability is low. A certain share of investors merely filtering out companies deemed "bad" doesn’t yet drive much change and shouldn’t necessarily warrant a green label for the fund, either.

Moreover, the basis for excluding individual industries might sometimes feel arbitrary. For example, fast food companies are typically not included in the list of harmful companies, while fossil fuel companies in need of transitions are outright excluded from the investment universe.

Definition 2: Incremental reduction of negative impacts

Another widely adopted approach is evaluating a company's sustainability based on its incremental reduction of negative impacts. This method's popularity stems from factors like enhanced disclosure data availability, propelled by initiatives such as SFDR, and a growing concern for issues like climate change and biodiversity. Some of the common methods for assessing the topic include company-disclosed adverse impact indicators such as CO2 emissions and climate pledges such as SBTi.

Tracking the largest negative impacts provides some clear benefits for a company, such as helping to drive CO2 reductions in operations. At the same time, focusing on negative impacts also presents a significant challenge when used to define sustainability for an investor: it often implies that incremental reductions suffice to make an investment a sustainable one.

However, reducing CO2 intensities doesn't equate to an absolute reduction in CO2 emissions globally, nor does it address the broader concept of holistic sustainability beyond the environment. Coca Cola or Meta setting SBTis or net zero targets and incrementally reducing their CO2 emission intensities doesn’t yet necessarily make their business models sustainable, but it may create an illusion of "taking action".

Definition 3: Evaluation of core business impact

If neither of the two previous dominant approaches seem to pass analytical scrutiny, what might work better, then?

An increasing number of forerunning institutional investors have started to evaluate a company's largest core business impacts to determine its sustainability. This entails assessing whether a company's activities generate more positive than negative value, taking environmental and social externalities into consideration. Or alternatively, whether a company is provenly transitioning towards this type of net positive state.

Using this definition can be done via various methodologies, such as classifying company revenues in a binary manner as sustainable or unsustainable, typically based on EU taxonomy or UN SDG specifications.

A more nuanced yet also more methodologically complex method includes quantification of companies’ holistic impacts, often in a monetary unit comparable across impacts, and optionally calculating the holistic net impact of a company.

More robust sustainability definitions and data may entail a major shift in classifying sustainable investments for investors.

While few investors seem to deny the relevance and importance of evaluating the impact of companies’ products and services, the approach still remains less discussed compared to the two other definitions discussed above. This is likely driven by operational challenges, like data availability.

However, a more profound underlying reason can also exist: adhering to more robust sustainability definitions and data may entail a major shift in investment classification for investors and also pose challenges for companies acknowledging the unsustainability of their business models – no matter how prominently they report on their internal emissions reductions.

The critical question remains: Will investors or companies themselves be able to realize and react to these discrepancies early enough, before their stakeholders like consumers, regulators, and the general public do it for them?

Want to dive deeper into defining sustainable investments?Download our on-demand webinar

Learn how the asset manager Aktia does Art 9 classification with Upright

March 28th, 2024

Upright Project

Share: